2021-9-15 17:00 |

This week, Bitcoin is back up over $47,000 again and Ethereum over $3,400 while the total crypto market cap is around $2.23 trillion.

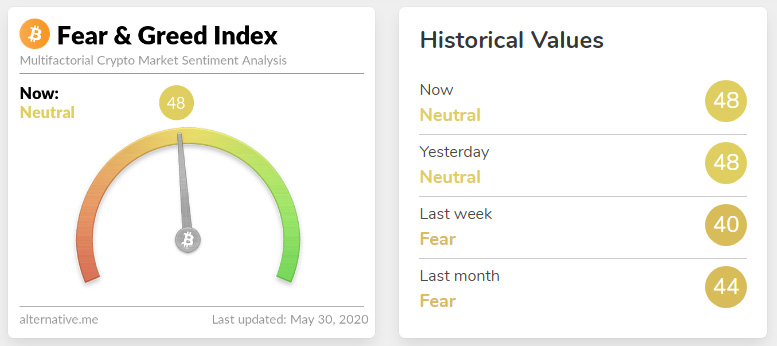

As price action in the market gets better again, so do the sentiments with the Crypto fear and Greed Index at “neutral” with a reading of 49, up from “fear” at 30 from yesterday.

When it comes to the network usage, over the past week following the flash crash, Bitcoin active addresses dropped to a 7-day average of 745.6k while adjusted transfer value increased by 21.6% for a daily average of over $10.1 bln.

As for Ether, active addresses increased by 5.6% as transactions began to dip to pre-August levels, with L2 solutions like Arbitrum gaining traction and NFT season dying down.

Network Usage Making RecoveryWhile active addresses fell on a weekly basis, unique monthly active users of large-caps are growing. Bitcoin’s monthly unique active addresses peaked at a little over 22.1 million in mid-January while weekly unique active addresses peaked in early January only to spike on May 8th but again topping at 6.7 mln.

In mid-July, these monthly unique active addresses fell to as low as 14.3 million following China's crackdown on cryptocurrency mining, leading to miners moving out of the country and moving overseas. But since then it has rebounded and climbed back above 16.5 million.

Coming onto Ether, its monthly active addresses topped a little over 13 million on May 18th following the first NFT boom and ETH price hitting a new ATH above $4k. After sliding to a low of 6.8 million, this downward trend finally appears to have started to reverse this month as it climbed back above 7 million late last week.

User Adoption Continues To GrowThe number of addresses holding at least one ten-billionth of the total supply of BTC and Ether has been on an incline as well.

While most of Bitcoins’ growth came at the beginning of the year, Ether’s came during the summer. Bitcoin had added over 1.5 million addresses by mid-April, and Ether has added 2.5 million addresses since May 1st.

When it comes to miner revenue, Bitcoin’s averaging $47 mln per day over the last month, 88% higher than June. However, miner revenue from fees is averaging 1.5% over the last 30 days, which is relatively low compared to the rest of 2021 so far.

As of ETH, which has been burning a portion of ETH fees ever since the London hard fork which implemented EIP 1559, one-third of its miners’ revenue generated from fees has fallen somewhat now that base fee is being burned but still, it has risen a little since.

“Priority fees (miner tips) have likely increased as a result of higher market volatility and continued NFT mania,” stated CoinMetrics in its report.

Stablecoin Adoption Hits New HighsMuch like the top networks, the usage of stablecoins also increased after last week’s crash, with USDC active addresses growing by 20% week-over-week. Unique monthly active users of major stablecoins, which reached a peak in mid-May, have started to rebound since mid-July as the market recovers.

Weekly active addresses of stablecoins hit their ATH in mid-May and decreased until mid-July, and are now recovering with the market.

Tether (USDT), by far the largest stablecoin in terms of weekly active addresses, issued on Tron (TRX), has been accounting for a majority of stablecoin weekly active addresses over the past six months.

Similarly, stablecoin adoption is back above pre-crash levels, with 7.5 million addresses holding at least $1 worth of stablecoins, a new all-time high, as of Sept. 11.

Stablecoin supply growth has also started to pick up again after a few months of flat to low growth. Adding more than 4 billion since Sept. 1st, much of which can be attributed to Tether, the total supply of stablecoins is now past 120 billion.

The post Ether Address Growth Surpasses Bitcoin, A Record 7.5 Million Addresses Holding at Least Worth of Stablecoins first appeared on BitcoinExchangeGuide. origin »Bitcoin price in Telegram @btc_price_every_hour

Bitcoin (BTC) на Currencies.ru

|

|